Visible rise in electricity distribution grid investment: ACER recommends actions to optimise the ramp-up

Visible rise in electricity distribution grid investment: ACER recommends actions to optimise the ramp-up

What is it about?

Today, ACER publishes its report on distribution system operator (DSO) investments and revenue setting.

The report:

- finds a major upscaling in electricity distribution grid investment trends across Europe;

- identifies some factors that may hinder efficient investments;

- reviews the DSO landscape in Europe;

- explores ways to address the challenges facing DSOs;

- proposes a set of 10 recommendations to optimise the ramp-up of distribution grid investment and improve services to grid user.

What are the main findings?

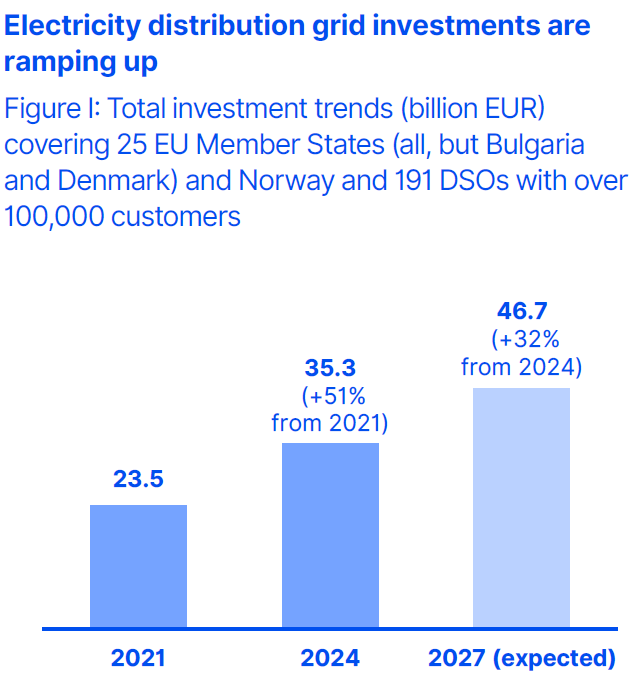

To accelerate decarbonisation, significantly more grid capacity is needed for electrification and renewables’ growth. This is driving a visible rise in electricity distribution grid investments across Europe. In 2024, annual distribution grid investments increased by over 50% to €35.3 billion (compared to €23.5 billion in 2021). Distribution grid investment is projected to approach €47 billion in 2027.

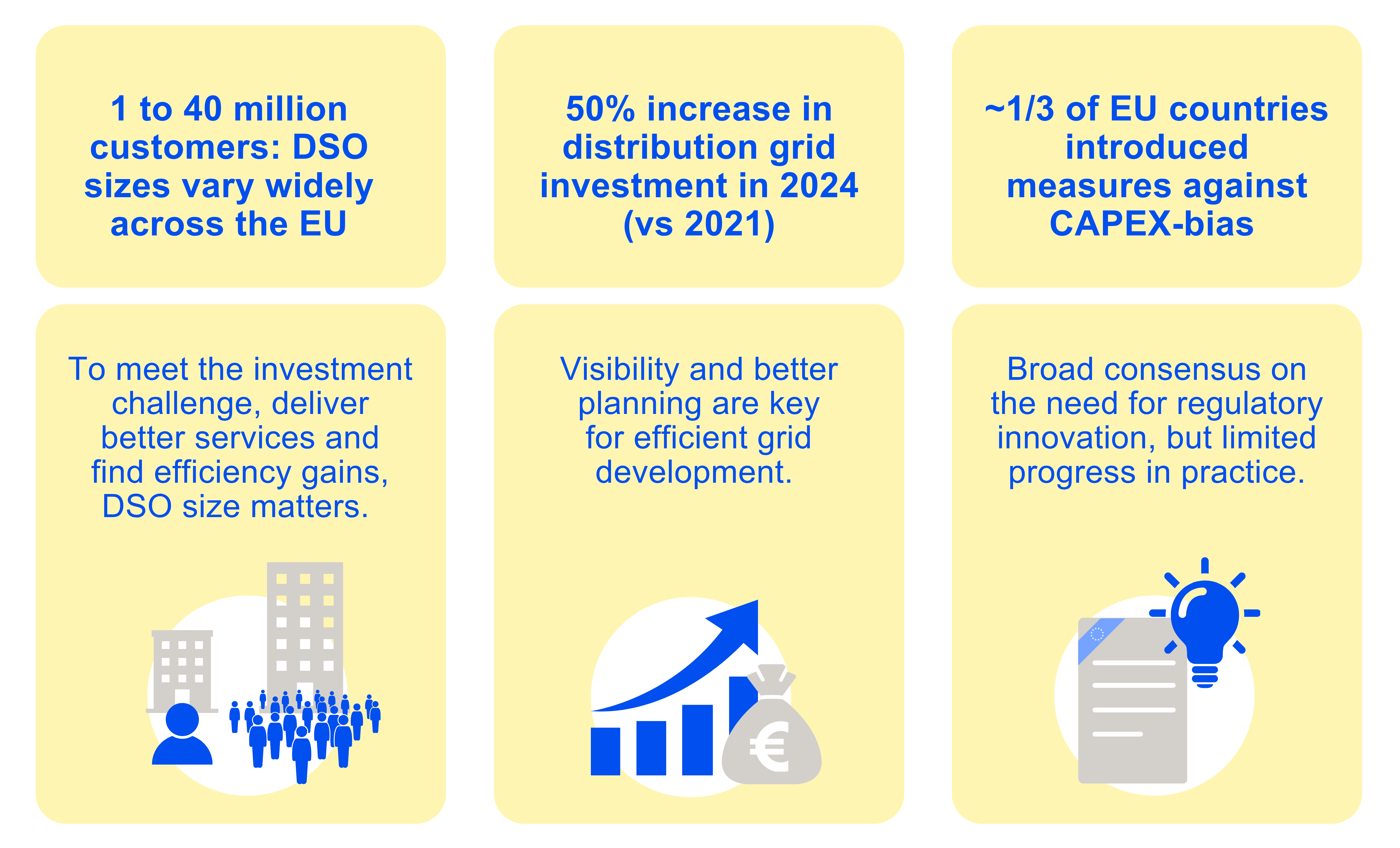

Beyond the investment challenge, DSOs face expanded roles under EU legislation. They must be active system operators (e.g. managing the system, utilising flexibility services, optimising electricity flows on the grid), market facilitators, data hubs, and innovation drivers – responsibilities that require new tools, specialised skills, and stronger coordination.

Europe needs DSOs who provide high quality distribution services. As the system evolves, regulatory frameworks must adapt alongside it.

This ACER report highlights several elements that might hinder efficient investments:

- Size matters. DSOs must be equipped to deal with evolving responsibilities for grid planning, flexibility solutions, grids’ digitalisation and resilience, to ensure all customers have equal access to high-quality and cost-efficient distribution services. Robust system planning and efficient regulatory scrutiny should not be compromised by fragmented and uncoordinated network development.

- DSOs should adopt the most efficient solutions for network development – whether grid-based or non-grid (e.g. flexibility). The regulatory focus must expand beyond cost-cutting and maximise the benefits for society. Reducing capital expenditure (CAPEX) bias, still present in several countries, is key for improving regulatory regimes.

- Rigid expenditure caps should not hinder nor distort key investments needed for the clean energy transition.

- Distribution grid use and planned development should be more transparent. DSOs should strive to publish their mid-term cost trajectories and monitor grid utilisation to improve planning and operations.

ACER’s report offers 10 recommendations for legislators, regulators and system operators to optimise the ramp-up of distribution grid investment and improve services to grid users. These aim to ensure adequate competences, proper transparency and unlock efficient investments. National regulatory authorities should consider these recommendations when setting or approving their distribution revenue methodologies.

What are the next steps?

ACER will continue to:

- facilitate best-practice sharing among national regulatory authorities; and

- engage with stakeholders to gather insights.

In 2027, ACER will publish the next edition of its report on network tariff practices. ACER’s next report on revenue setting practices will be in 2028.